Don’t Expect a Flood of Foreclosures

The rising cost of just about everything from groceries to gas right now is leading to speculation that more people won’t be able to afford their mortgage payments. And that’s creating concern that a lot of foreclosures are on the horizon. While it’s true that foreclosure filings have gone up a bit compared to last year, experts say a flood of foreclosures isn’t coming.

Take it from Bill McBride of Calculated Risk. McBride is an expert on the housing market, and after closely following the data and market environment leading up to the crash, he was able to see the foreclosures coming in 2008. With the same careful eye and analysis, he has a different take on what’s ahead in the current market:

“There will not be a foreclosure crisis this time.”

Let’s look at why another flood is so unlikely.

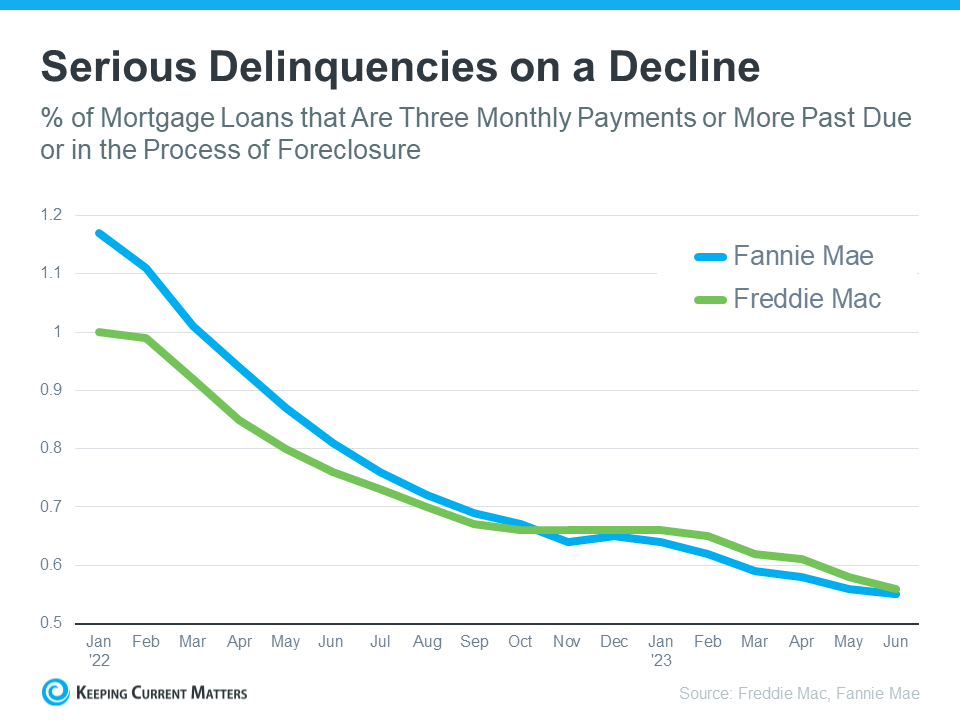

There Aren’t Many Homeowners Who Are Seriously Behind on Their Mortgage Payments

One of the main reasons there were so many foreclosures during the last housing crash was because relaxed lending standards made it easy for people to take out mortgages, even if they couldn’t show that they’d be able to pay them back. At that time, lenders weren’t being very strict when assessing applicant credit scores, income levels, employment status, and debt-to-income ratio.

But now, lending standards have tightened, leading to more qualified buyers who can afford to make their mortgage payments. And data from Freddie Mac and Fannie Mae shows the number of homeowners who are seriously behind on their mortgage payments is declining (see graph below):

Molly Boese, Principal Economist at CoreLogic, explains just how few homeowners are struggling to make their mortgage payments:

Molly Boese, Principal Economist at CoreLogic, explains just how few homeowners are struggling to make their mortgage payments:

“May’s overall mortgage delinquency rate matched the all-time low, and serious delinquencies followed suit. Furthermore, the rate of mortgages that were six months or more past due, a measure that ballooned in 2021, has receded to a level last observed in March 2020.”

Before there can be a significant rise in foreclosures, the number of people who can’t make their mortgage payments would need to rise. Since so many buyers are making their payments today, a wave of foreclosures isn’t likely.

Bottom Line

In conclusion, if the thought of an impending wave of foreclosures has been causing you concern, rest assured that the latest data offers a more optimistic perspective. The real estate landscape, particularly in the stunning Telluride region, remains robust and resilient. At Mountain Rose Realty, we're here to provide you with insights and guidance into the Telluride real estate market.

With Anne-Britt and our dedicated team, your journey through the Telluride homes for sale becomes an exciting exploration of possibilities. As qualified buyers consistently demonstrate their commitment by staying current on mortgage payments, the stability of the market shines through.

So, whether you're in search of Telluride real estate, aiming to discover your dream mountain getaway, or considering homes for sale in Telluride, CO, remember that the outlook remains promising. Feel free to reach out to us at Mountain Rose Realty for expert assistance in navigating this vibrant market. Your vision of Telluride living is closer than ever, and we're here to help transform it into a reality.

Frequently Asked Questions

- Are foreclosures expected to flood the market in 2023?

- No. While foreclosure filings have risen slightly compared to last year, experts like Bill McBride of Calculated Risk—who accurately predicted the 2008 crisis—forecast that there will not be a foreclosure crisis this time. The current market conditions are fundamentally different from the pre-2008 environment.

- Why are fewer foreclosures expected now compared to 2008?

- Lending standards have tightened significantly since 2008, making it harder for unqualified buyers to obtain mortgages. Today's lenders carefully assess credit scores, income, employment status, and debt-to-income ratios, resulting in more qualified homeowners who can afford their payments.

- What does the current mortgage delinquency data show?

- As of May 2023, the overall mortgage delinquency rate matched an all-time low, and serious delinquencies did as well. The rate of mortgages six months or more past due has fallen to levels not seen since March 2020, indicating homeowners are staying current on payments.

- What would need to happen for foreclosures to significantly rise?

- For a wave of foreclosures to occur, the number of homeowners unable to make mortgage payments would need to rise substantially. Since the majority of today's qualified buyers are making their payments reliably, this scenario is unlikely.